Alright. So, after you've completed your bank reconciliation, you need to make journal entries for all of the items in the book column. Let's see how that works. So, just like I said, we have to make journal entries for every item in the book column. Okay. So, the book column, right, we had some amount of cash and then we found all these things that had affected the cash account that we had not taken journal entries for yet.

Let's see, the bank collection. If the bank collects money on our behalf, that's usually some situation where a customer owes us money and they're finally paying us. So, the journal entry is going to look something like this. Debit cash because we received cash, I'll just put x's for the amount and we're gonna credit accounts receivable, AR, right? Because it’s a customer that's paying us, so we decrease the balance in accounts receivable and we receive the cash.

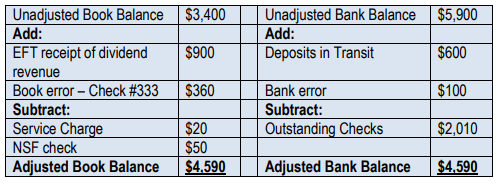

Okay. So, this all happens with the bank reconciliation. After you've made the bank reconciliation, you make these journal entries depending on which items showed up during your reconciliation.

Electronic funds transfer. Okay. So, if you received an electronic funds transfer, that's usually something that generally a customer paid you or something. So, it would be the same as bank collections and we would see something like this. Cash and AR just like above, right? We received cash and we reduce our accounts receivable from a customer. But if it's an EFT payment, the situation where we paid somebody, well that would be cash leaving our account, right? So we would be paying off something like accounts payable, we would debit accounts payable a liability, right? So, that would reduce our liability by debiting it and we would credit cash to reduce our cash.

Next is a service charge. So, this is where the bank charges us a fee. So, what happens when the bank charges a fee? We take an expense, right, we had some sort of expense and it would be something like, you know, bank fee expense, right? Whatever it might be. Could be bank fee expense, you know, service charges, whatever you want to call the expense account. You would debit that, right, to increase the expense and we would credit cash because it came out of our cash, right? The bank took it out of our bank account, so we have to reduce cash.

Interest revenue. In this case, we're receiving cash, right? The bank is paying us cash for our balance. So we debit cash because we receive cash and we're gonna credit what do we credit in this case? We're gonna credit interest revenue, right? We earned interest, we earned it during this period, we earned revenue. So we're gonna credit interest revenue, revenues go up with a credit, so that's good. We received cash from interest revenue.

How about not sufficient funds checks? So, NSF checks, this one's a little tricky. You have to think about what we did in the past. In the past, so I'm actually going to draw it here. So I'll do it in parenthesis. In the past, we might have made a journal entry that looked like this. Oh, we received a check from a customer. Great. Let's make a journal entry because we received this check. We would say, okay we received cash from this customer and he no longer owes us this money. Right? So, we would have made this entry sometime in the past when we received the check and now we're looking at the bank statement and they said, hey, that check bounced. That's not fair. We didn't get that money from the customer and we were supposed to. Well, that customer still owes us that money in this case. So what we have to do is reverse this entry. We're going to debit accounts receivable, so now what we do is we debit accounts receivable for whatever that amount was and we credit cash, right? Because what happened is before we thought we had received this cash. So before we thought we had received this cash, so we had increased our cash balance but now we're realizing here we are.

Alright, so the last thing here is book errors. Okay? Here we are. Alright. So the last thing here is book errors. Okay. Book errors are going to be really tough for me to tell you, so you just have to remove the effects there. Okay, you have to remove the effects of the error and it generally has to do with something like thinking how we did with the NSF checks. We have to think about the entry we would have originally made and then the correct entry and then we have to make it correct, right? We have to take it from the incorrect error entry to the correct entry and find out what would get us there. Okay? So that is how we make the journal entries.

Let's go ahead and pause and we'll make the journal entries from our practicing, BankRight. Alright, let's do it now.