10. The Costs of Production

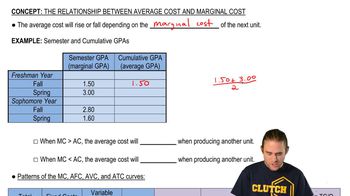

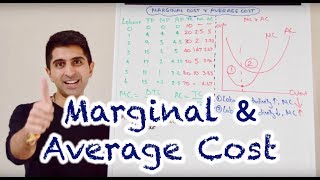

The Relationship Between Average Cost and Marginal Cost

Multiple Choice

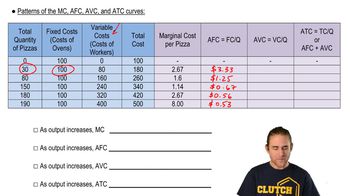

Multiple ChoiceA firm is currently producing 100 units with an average total cost of $44 and a marginal cost of $32. If it were to increase production to 101 units, which of the following must be true?

A

Average total cost would decrease.

B

Average total cost would increase.

C

Marginal cost would decrease.

D

Marginal cost would increase.

442

views

1

rank

1

comments

Related Videos

Related Practice

06:38

06:38

Showing 1 of 7 videos