Table of contents

- 0. Basic Principles of Economics

- Introduction to Economics

- People Are Rational

- People Respond to Incentives

- Scarcity and Choice

- Marginal Analysis

- Allocative Efficiency, Productive Efficiency, and Equality

- Positive and Normative Analysis

- Microeconomics vs. Macroeconomics

- Factors of Production

- Circular Flow Diagram

- Graphing Review

- Percentage and Decimal Review

- Fractions Review

- 1. Reading and Understanding Graphs

- 2. Introductory Economic Models

- 3. The Market Forces of Supply and Demand

- Competitive Markets

- The Demand Curve

- Shifts in the Demand Curve

- Movement Along a Demand Curve

- The Supply Curve

- Shifts in the Supply Curve

- Movement Along a Supply Curve

- Market Equilibrium

- Using the Supply and Demand Curves to Find Equilibrium

- Effects of Surplus

- Effects of Shortage

- Supply and Demand: Quantitative Analysis

- 4. Elasticity

- Percentage Change and Price Elasticity of Demand

- Elasticity and the Midpoint Method

- Price Elasticity of Demand on a Graph

- Determinants of Price Elasticity of Demand

- Total Revenue Test

- Total Revenue Along a Linear Demand Curve

- Income Elasticity of Demand

- Cross-Price Elasticity of Demand

- Price Elasticity of Supply

- Price Elasticity of Supply on a Graph

- Elasticity Summary

- 5. Consumer and Producer Surplus; Price Ceilings and Floors

- Consumer Surplus and Willingness to Pay

- Producer Surplus and Willingness to Sell

- Economic Surplus and Efficiency

- Quantitative Analysis of Consumer and Producer Surplus at Equilibrium

- Price Ceilings, Price Floors, and Black Markets

- Quantitative Analysis of Price Ceilings and Price Floors: Finding Points

- Quantitative Analysis of Price Ceilings and Price Floors: Finding Areas

- 6. Introduction to Taxes and Subsidies

- 7. Externalities

- 8. The Types of Goods

- 9. International Trade

- 10. The Costs of Production

- 11. Perfect Competition

- Introduction to the Four Market Models

- Characteristics of Perfect Competition

- Revenue in Perfect Competition

- Perfect Competition Profit on the Graph

- Short Run Shutdown Decision

- Long Run Entry and Exit Decision

- Individual Supply Curve in the Short Run and Long Run

- Market Supply Curve in the Short Run and Long Run

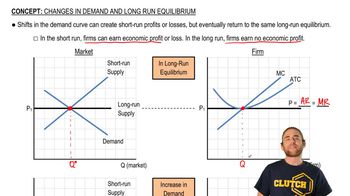

- Long Run Equilibrium

- Perfect Competition and Efficiency

- Four Market Model Summary: Perfect Competition

- 12. Monopoly

- 13. Monopolistic Competition

- 14. Oligopoly

- 15. Markets for the Factors of Production

- 16. Income Inequality and Poverty

- 17. Asymmetric Information, Voting, and Public Choice

- 18. Consumer Choice and Behavioral Economics

11. Perfect Competition

Long Run Equilibrium

11. Perfect Competition

Long Run Equilibrium

07:04

07:04

Practice this topic

- Multiple Choice

If the price is P1, the firms are

720views4rank - Multiple Choice

Suppose the cost curves apply to all firms in the industry. If the initial price is P1, in the long run, the market

725views4rank - Multiple Choice

A new study shows that eating raw garlic keeps vampires away (vampires have become a huge problem). This news shifts the demand curve for raw garlic to the right. In response, new firms enter the garlic market. While firms are entering the market, the price of raw garlic ____________ and the profit of each existing firm _____________.

690views5rank - Multiple ChoiceWhich of the following must be true in the long run equilibrium for a perfectly competitive market?115views