12. Monopoly

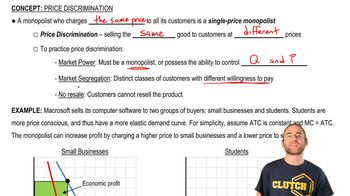

Price Discrimination

Struggling with Microeconomics?

Join thousands of students who trust us to help them ace their exams!Watch the first videoMultiple Choice

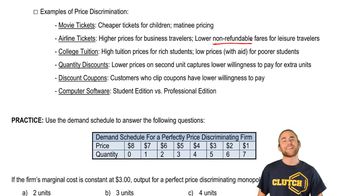

If the firm's marginal cost is constant at $3.00, output for a perfect price discriminating monopolist is:

A

2 units

B

3 units

C

4 units

D

5 units

Verified step by step guidance

Verified step by step guidance1

Understand that a perfectly price discriminating monopolist charges each consumer the maximum price they are willing to pay for each unit, which is reflected in the demand schedule.

Identify the marginal cost (MC) of production, which is given as $3.00. This is the cost of producing one more unit of output.

To determine the output level, compare the marginal cost to the price each unit can be sold for, as shown in the demand schedule. The firm will produce and sell units as long as the price is greater than or equal to the marginal cost.

Examine the demand schedule: the firm can sell the first unit for $8, the second for $7, the third for $6, the fourth for $5, and the fifth for $4. All these prices are above the marginal cost of $3.00.

Conclude that the firm will produce and sell up to the point where the price equals or exceeds the marginal cost. In this case, the firm will produce 5 units, as the price for the fifth unit ($4) is still above the marginal cost ($3).

7:45m

7:45mWatch next

Master Price Discrimination with a bite sized video explanation from Brian Krogol

Start learningRelated Videos

Related Practice