13. Monopolistic Competition

Monopolistic Competition in the Long Run

Struggling with Microeconomics?

Join thousands of students who trust us to help them ace their exams!Watch the first videoMultiple Choice

New firms will enter a monopolistically competitive market if

A

Marginal revenue is greater than marginal cost

B

Marginal revenue is greater than average total cost

C

Price is greater than marginal cost

D

Price is greater than average total cost

Verified step by step guidance

Verified step by step guidance1

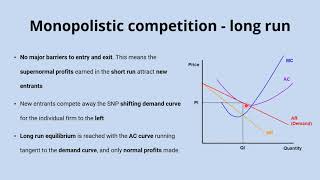

Understand the characteristics of a monopolistically competitive market: Many firms, differentiated products, and free entry and exit in the long run.

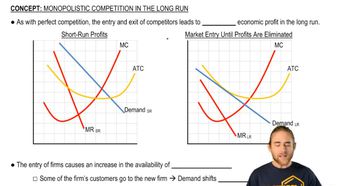

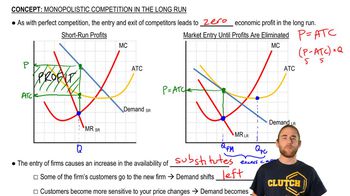

Recall that in the long run, firms in a monopolistically competitive market will earn zero economic profit due to the entry of new firms.

Identify the condition for new firms to enter the market: New firms will enter if existing firms are making economic profits.

Economic profit occurs when total revenue is greater than total cost. In terms of per-unit measures, this means that the price (P) must be greater than the average total cost (ATC).

Therefore, the correct condition for new firm entry is when the price is greater than the average total cost (P > ATC), indicating that existing firms are earning positive economic profits.

9:47m

9:47mWatch next

Master Monopolistic Competition in the Long Run with a bite sized video explanation from Brian Krogol

Start learningRelated Videos

Related Practice