18. Consumer Choice and Behavioral Economics

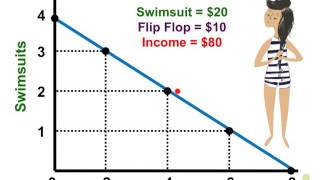

Budget Constraint

Struggling with Microeconomics?

Join thousands of students who trust us to help them ace their exams!Watch the first videoMultiple Choice

Campin' Sam buys firewood and ice. When the price of firewood decreases, the maximum number of firewood she can purchase _____________ and the maximum number of ice she can purchase _______________

A

Increases; increases

B

Increases; decreases

C

Decreases; increases

D

Increases; remains constant

E

Remains constant; remains constant

Verified step by step guidance

Verified step by step guidance1

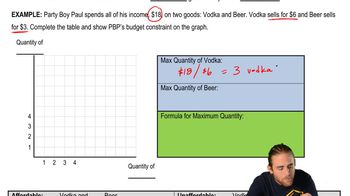

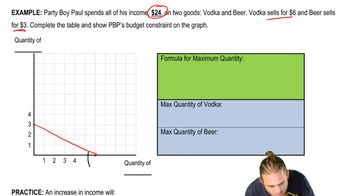

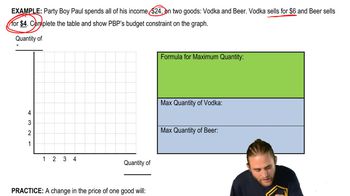

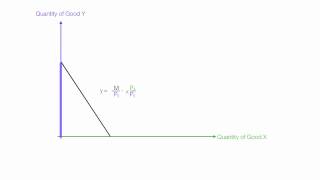

Understand the concept of a budget constraint: A budget constraint represents all the combinations of goods and services that a consumer can purchase given their income and the prices of those goods and services.

Consider the effect of a price change on the budget constraint: When the price of one good (firewood) decreases, the consumer can afford to buy more of that good with the same amount of money, effectively increasing the maximum quantity of firewood that can be purchased.

Analyze the impact on the other good (ice): Since the price of ice has not changed, the maximum quantity of ice that can be purchased remains constant, assuming the consumer's income and the price of ice remain unchanged.

Visualize the budget line: The budget line pivots outward from the axis representing firewood, indicating that more firewood can be purchased, while the intercept on the ice axis remains the same.

Conclude the effect on purchasing power: The decrease in the price of firewood increases the consumer's purchasing power for firewood, but does not affect the purchasing power for ice, leading to the conclusion that the maximum number of firewood increases while the maximum number of ice remains constant.

8:41m

8:41mWatch next

Master Budget Constraint (Budget Line) with a bite sized video explanation from Brian Krogol

Start learningRelated Videos

Related Practice