Table of contents

- 1. Introduction to Macroeconomics2h 3m

- 2. Introductory Economic Models1h 9m

- 3. Supply and Demand3h 23m

- Introduction to Supply and Demand4m

- The Basics of Demand6m

- Individual Demand and Market Demand3m

- Shifting Demand38m

- The Basics of Supply2m

- Individual Supply and Market Supply6m

- Shifting Supply28m

- Overview of Supply and Demand Shifts7m

- Supply and Demand Together: Equilibrium, Shortage, and Surplus8m

- Supply and Demand Together: One-sided Shifts20m

- Supply and Demand Together: Both Shift34m

- Supply and Demand: Quantitative Analysis40m

- 4. Elasticity2h 25m

- Percentage Change and Price Elasticity of Demand18m

- Elasticity and the Midpoint Method20m

- Price Elasticity of Demand on a Graph11m

- Determinants of Price Elasticity of Demand6m

- Total Revenue Test13m

- Total Revenue Along a Linear Demand Curve14m

- Income Elasticity of Demand23m

- Cross-Price Elasticity of Demand11m

- Price Elasticity of Supply12m

- Price Elasticity of Supply on a Graph3m

- Elasticity Summary9m

- 5. Consumer and Producer Surplus; Price Ceilings and Price Floors3h 11m

- WIllingness to Pay and Consumer Surplus18m

- Willingness to Sell and Producer Surplus12m

- Economic Surplus and Efficiency18m

- Quantitative Analysis of Consumer and Producer Surplus at Equilibrium28m

- Price Ceilings, Price Floors, and Black Markets38m

- Quantitative Analysis of Price Ceilings and Floors: Finding Points20m

- Quantitative Analysis of Price Ceilings and Floors: Finding Areas54m

- 6. Introduction to Taxes1h 29m

- 7. Externalities54m

- 8. The Types of Goods1h 3m

- 9. International Trade1h 16m

- 10. Measuring National Output and Income 54m

- 11. Unemployment and Inflation1h 34m

- Labor Force and Unemployment10m

- Types of Unemployment12m

- Unemployment: Minimum Wage Laws and Efficiency Wages7m

- Inflation and Consumer Price Index (CPI)16m

- Using CPI to Adjust for Inflation7m

- Problems with the Consumer Price Index (CPI)5m

- Nominal Income and Real Income12m

- Nominal Interest, Real Interest, and the Fisher Equation5m

- Who is Affected by Inflation?5m

- Demand-Pull and Cost-Push Inflation6m

- Costs of Inflation: Shoe-leather Costs and Menu Costs4m

- 12. Productivity and Economic Growth1h 4m

- 13. The Financial System1h 30m

- 14. Income and Consumption57m

- 15. Deriving the Aggregate Expenditures Model1h 14m

- 16. Aggregate Demand and Aggregate Supply Analysis1h 22m

- Aggregate Demand17m

- Deriving Aggregate Demand from the Aggregate Expenditure Model12m

- Shifting Aggregate Demand4m

- Long Run Aggregate Supply9m

- Short Run Aggregate Supply7m

- Shifting Short Run Aggregate Supply8m

- AD-AS Model: Equilibrium in the Short Run and Long Run5m

- AD-AS Model: Shifts in Aggregate Demand18m

- 17. The Monetary System58m

- The Functions of Money; The Kinds of Money8m

- Defining the Money Supply: M1 and M22m

- Required Reserves and the Deposit Multiplier8m

- Introduction to the Federal Reserve8m

- The Federal Reserve and the Money Supply11m

- History of the US Banking System9m

- The Financial Crisis of 2007-2009 (The Great Recession)10m

- 18. Monetary Policy1h 26m

- 19. Fiscal Policy52m

- 20. Tradeoffs Between Inflation and Unemployment1h 2m

- 21. Open-Economy Macroeconomics1h 44m

- Balance of Payments: Introduction5m

- Balance of Payments: Current Account8m

- Balance of Payments: Financial Account and Capital Account7m

- Net Exports Equal Net Foreign Investment7m

- Balance of Trade; Trade Deficit and Trade Surplus6m

- Exchange Rates: Introduction14m

- Exchange Rates: Nominal and Real13m

- Exchange Rates: Equilibrium8m

- Exchange Rates: Shifts in Supply and Demand11m

- Exchange Rates and Net Exports6m

- Exchange Rates: Purchasing Power Parity3m

- The Gold Standard4m

- The Bretton Woods System6m

- 22. Macroeconomic Schools of Thought40m

- 23. Dynamic AD/AS Model32m

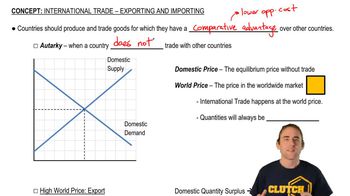

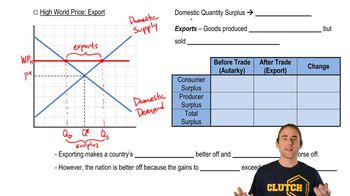

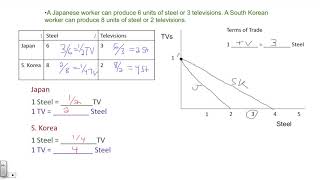

9. International Trade

Exporting and Importing

Low World Price: Import

Brian Krogol

Video duration:

6mPlay a video:

Related Videos

Related Practice

02:56

02:56